Embedded payments are reshaping how businesses take money, settle accounts, and serve customers. Instead of sending people to third parties, payment flows live inside the tools you already use.

This guide breaks down what embedded payments are, why they matter, and how they remove friction from daily work. You will see how they help with checkout, cash flow, fraud, and customer experience.

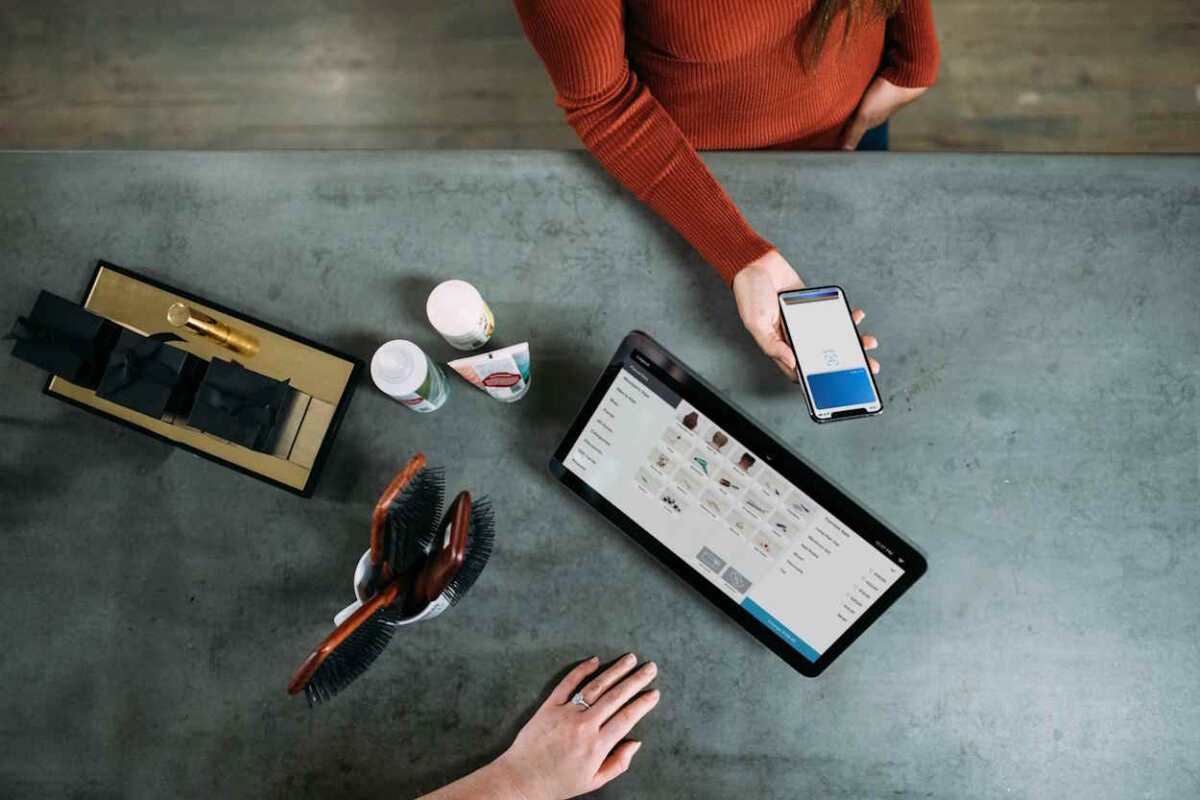

What Are Embedded Payments

Embedded payments place payment capabilities directly inside your software, website, or app. Customers transact without hopping between tabs or typing the same details again and again.

For teams, this means fewer moving parts. Payment acceptance becomes a built-in function tied to inventory, CRM, and reporting, not a standalone task with manual handoffs.

Developers also benefit. SDKs, tokenization, and unified APIs simplify builds so new payment options can ship faster. That speed helps you meet customer demand without heavy custom code.

Why Simpler Checkouts Matter

Checkout is your last mile. Every extra click adds risk of dropoff, and small delays stack into real revenue loss.

Many businesses fix this by trimming fields and auto-filling data – then adding trusted wallets and stored credentials to cut time further. When embedded in your checkout, Xplor Pay supports smooth user flow and upholds compliance and security. The result is fewer abandoned carts and fewer support tickets about failed payments.

Reducing Manual Work Across Teams

Without embedded payments, finance and ops often chase details across gateways, spreadsheets, and emails. That drains hours and introduces errors.

With an embedded approach, settlement data flows into the systems your teams already use. Refunds, partial captures, and subscriptions become routine clicks instead of one-off projects.

Support improves, too. Agents can see order status, payment state, and fulfillment in one place, which shortens calls and raises first-contact resolution.

Improving Cash Flow And Reconciliation

Cash flow loves speed and predictability. Embedded payments can speed funding and give clearer visibility into what cleared, what is pending, and what needs attention.

Clean reconciliation follows. When transactions, fees, and payouts align with orders in your core system, the month-end close is smoother, and audits are less painful.

Clear reporting helps leaders plan. Forecasts get better when you trust the numbers and can slice by product, channel, and customer segment.

Lowering Fraud Risk Without Friction

Security is not just about blocking bad actors – it is about keeping good customers moving. Embedded payment tools combine on-device signals, tokenization, and step-up checks to do both.

A Mastercard whitepaper noted that embedding card-on-file experiences with seamless authentication can reduce fraud while improving conversion, particularly when shoppers recognize consistent checkout patterns. That balance keeps approvals high and chargebacks low.

As rules evolve, built-in compliance updates help you keep pace. Your team spends less time decoding standards and more time building value.

Creating Better Customer Experiences

Customers want familiar, fast, and flexible ways to pay. Embedded payments let you offer cards, wallets, pay-by-link, and subscriptions in one place.

Loyalty can sit right beside payments. Points apply at checkout, rewards trigger automatically, and customers see real-time balances without leaving the flow.

Post-purchase touchpoints improve as well. Receipts, invoices, and order updates stay consistent across channels, which builds trust and reduces confusion.

How To Get Started Without The Headaches

Begin with your current stack. Map the systems that touch payments today and list the pain points your teams feel most.

Pick one high-impact journey to embed first – often checkout or in-app renewals. Keep the scope tight so you can learn fast, tune the experience, and prove value.

Then scale by adding methods, markets, and use cases. Watch metrics like approval rate, checkout time, refund speed, and support contacts to track gains.

Choosing The Right Partner

Look for a provider that offers clean APIs, clear documentation, and strong developer tools. Reliable sandboxes and sample apps will speed your first launch.

Prioritize security features that do not slow users down. Tokenization, vaulting, and adaptive authentication should be table stakes, along with clear dispute workflows.

Assess reporting depth and data access. You should be able to export, pipe to your BI tool, and build dashboards without hacks.

Measuring What Matters

Set baselines before you switch. Know your current approval rate, time-to-pay, chargeback rate, and average time to reconcile.

After embedding, compare weekly for the first 8 weeks. Look for lift in conversion, fewer support tickets, and faster close cycles.

Share results across teams. When finance, product, and support see the same gains, it is easier to expand the program.

Modern payment workflows do not have to be complex. With embedded payments, you can reduce busywork, raise conversion, and gain clearer control over cash.

Adopt a staged approach, measure results, and keep the user journey front and center. Small steps add up to a smoother business and happier customers.